Alarm Bells are Ringing! Could we be Entering Recession Territory?

By Brad Lamensdorf and John Del Vecchio

The yield curve is inverting, which means that long-term interest rates might start to trade below short-term interest rates. If the past is any indicator of the future, it could mean that we are staring a recession in the face. If investors are concerned about the economy, they may prefer to hold longer-term treasuries that yield less than short-term treasuries. Obviously, this makes no sense in a perfect world. But, in the real, world if investors think a recession is coming they don’t want to own short-term treasuries that ultimately will see their yield fall. They’d rather get locked into a lower rate now that may end up being higher when short-term rates tank as the result of a recession.

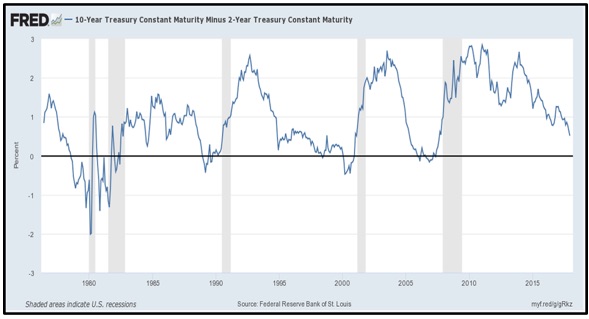

A look at the chart below shows that the recent trend between the 10-year treasury and the 2-year treasury (blue line) is nosediving toward the zero line. The grey shaded areas in the chart show past recessions. Typically, when the yield curve implodes, a recession has been close by.

It’s not always immediate. Look back at the 1990’s, when it took a while for a recession to rear its ugly head. The wealth effect from the boom in technology may have shielded some of the impact of the negative yield curve, but eventually the economy got bit. Bit hard.

Now you can see that we are trending down to multi-year lows. The difference today is that there’s a boatload of leverage in the system. Leverage is great while it’s working…until it isn’t. Then some bad things can happen.

For example, many financial institutions set up trades, called derivatives, that depend on a positive interest rate carry (blue line above trending up) to be profitable. These trades may have been set up a couple of years ago, and the bank may have misjudged the future of the yield curve. As these trades go against them, it does huge damage to their balance sheet. Not only are they no longer profitable, but the addition to leverage adds fuel to the fire. There’s a reason why Warren Buffett has called these type of trades “financial weapons of mass destruction”. We could see another wave of massive write-downs or bank failures just like we saw 10 short years ago, for many of the same reasons. People have short memories!

Another scenario is that short-term loans on long-term assets could lead to the consistency of payments to a bank to fluctuate wildly. Let’s say someone owns a building that is financed with short-term loans that are often refinanced because rates have trended lower, and the building generates $100,000 in rent. If the economy gets hit by a recession, the building owner might see his cash flow evaporate as tenants go under and close up shop. Now the bank might get stuck with a default. Meanwhile, the bank can’t borrow money at short-term rates and loan it out longer-term for higher rates. Loan growth slows and margins take a hit. The result is bad all around.

The concern is that “this time it’s different” and there won’t be problems. It’s never different this time. Human nature never changes. What’s more is that we cannot believe the economic growth or job statistics reported by the government. There’s all sorts of voodoo math in those figures. We should all position our investments accordingly.