Overpriced and Overbought

By John Del Vecchio and Brad Lamensdorf

The first half of 2022 was the worst start of the year for stocks in five decades.

There could be much more damage to come.

While equity returns were poor, we started the year with nosebleed valuations.

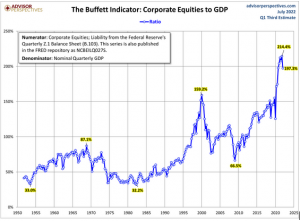

As the chart below from Advisor Perspectives shows, the Buffett Equity to GDP indicator topped out at 214%, a historical high. Even after a good beating in stocks, the indicator only fell to 197.3%

Also, a historically high level.

New bull markets are unlikely to start from such a high level.

Speculative stocks have had a good run the past couple of weeks. However, we think this is indicative of a bear market rally.

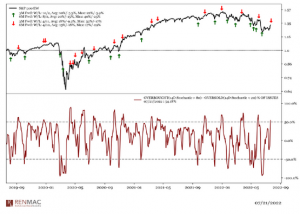

Right on cue, stocks have become very overbought while valuations remain rich.

The following chart from RENMAC illustrates that we have not hit overbought levels. Typically, returns from here are poor until the overbought condition is worked off.

In our view, it is a good time to add back hedges.

To learn more about how these indicators can help manage risk in your portfolio, book a call with Brad. You may book a call here.

DISCLOSURE: LAMENSDORF MARKET TIMING REPORT

Lamensdorf Market Timing Report is a publication intended to give analytical research to the investment community. Lamensdorf Market Timing Report is not rendering investment advice based on investment portfolios and is not registered as an investment advisor in any jurisdiction. Information included in this report is derived from many sources believed to be reliable but no representation is made that it is accurate or complete, or that errors, if discovered, will be corrected. The authors of this report have not audited the financial statements of the companies discussed and do not represent that they are serving as independent public accountants with respect to them. They have not audited the statements and therefore do not express an opinion on them. The authors have also not conducted a thorough review of the financial statements as defined by standards established by the AICPA.

This report is not intended, and shall not constitute, and nothing herein should be construed as, an offer to sell or a solicitation of an offer to buy any securities referred to in this report, or a “buy” or “sell” recommendation. Rather, this research is intended to identify issues portfolio managers should be aware of for them to assess their own opinion of positive or negative potential. The LMTR newsletter is NOT affiliated with any ETF’s. Active Alts is affiliated with Lamensdorf Market Timing Report. While LMTR uses charts from SentimenTrader, they do not have a financial arrangement with SentimenTrader Past performance is not indicative of future results.